Mar 23, 2026

Employee Loans and Deductions in Philippine Payroll

How to manage SSS loans, Pag-IBIG loans, cash advances, and recurring deductions in Philippine payroll without losing track of balances.

One of your baristas took an SSS salary loan six months ago. Another one has a Pag-IBIG multi-purpose loan and a ₱2,000 cash advance from last month. You're running payroll tonight, and you're trying to remember: how many months are left on the SSS loan? Did you already deduct the cash advance last cutoff, or was that the cutoff before?

If you've been there, you know how quickly loan tracking gets messy. The deductions are straightforward one at a time. It's when you're managing multiple loans across multiple people across semi-monthly cutoffs that things fall through the cracks.

Why loans show up in payroll

When a staff member takes a loan from SSS or Pag-IBIG, the employer is responsible for deducting the monthly amortization from payroll and remitting it to the agency. That's not optional. SSS and Pag-IBIG expect the employer to be the collection channel, and missing a remittance creates problems for both the business and the staff member's loan record.

Company cash advances work the same way mechanically. You agreed to lend the money, and you recover it through payroll deductions over an agreed number of cutoffs. The difference is there's no government agency involved, just an agreement between you and your team member.

The common loan types

SSS salary loan

SSS members borrow against their contributions. Repayment runs 24 months through payroll deductions. The employer deducts the monthly amortization and remits it to SSS along with regular contributions.

SSS calamity loan

Available during declared calamities, with faster processing and lower interest. Same payroll deduction setup. If a staff member already has an outstanding salary loan, the calamity loan balance is tracked separately.

Pag-IBIG multi-purpose loan (MPL)

Based on savings and membership tenure. Repayment is up to 24 months. The employer deducts and remits to Pag-IBIG, same as SSS.

Pag-IBIG calamity loan

Similar to the SSS version but through Pag-IBIG. Available in areas hit by declared calamities, with the same payroll deduction terms.

Company cash advances

Internal arrangements between the business and the staff member. You set the terms: amount, monthly deduction, number of cutoffs. No agency involved, but you still need written authorization before deducting.

What the law says about deductions

Article 113 of the Labor Code limits when an employer can deduct from wages. Only three cases are allowed: when authorized by law (SSS, PhilHealth, Pag-IBIG, BIR), when authorized in writing by the staff member, or when required by a collective bargaining agreement.

For loans, this means you need written authorization before deducting. Even for government loans where you're the remitting agent, having the staff member acknowledge the deduction schedule is good practice and protects both sides.

There's also a practical limit. After mandatory contributions, tax, and all loan deductions, the person should still take home enough to live on. DOLE has taken the position that deductions should not reduce take-home pay to an unreasonable amount. If someone has three active loans and the combined deductions eat most of their pay, that's worth addressing before it becomes a formal complaint.

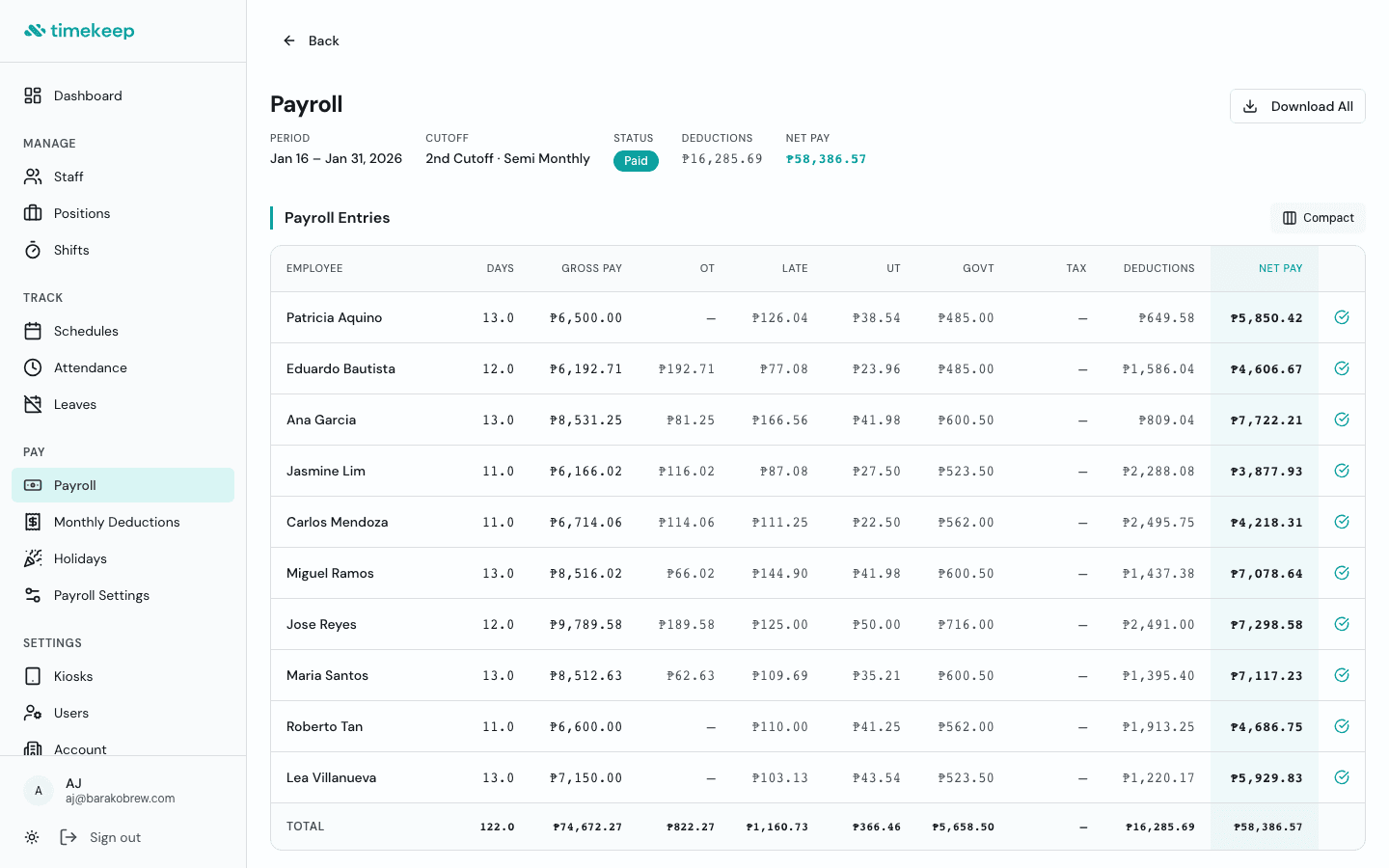

Where tracking breaks down

Each loan has three numbers: the principal (total borrowed), the monthly amortization (fixed payment per month), and the remaining balance. Every month, the amortization comes out. The balance goes down. When it hits zero, deductions stop.

Simple enough for one person with one loan. But five staff members with two loans each, across semi-monthly cutoffs, means 20 deduction lines changing every month. That's where the common mistakes happen.

Deducting after a loan is paid off. Without balance tracking, you might deduct for 26 months on a 24-month loan. The staff member overpays, and you owe them a refund.

Forgetting to start deductions on a new loan. The SSS notice sits in your inbox for two weeks. By the time you add it to payroll, you've missed a cutoff and need to catch up.

Getting the final deduction wrong. If the remaining balance is ₱300 but the regular amortization is ₱500, the last deduction should be ₱300. Deducting the full ₱500 means you owe ₱200 back.

Loans vs monthly deductions

Besides loans, businesses often have recurring monthly deductions: uniform charges, meal plan fees, health insurance top-ups, or company benefit premiums. These don't have a principal or a declining balance. They repeat every month until you remove them.

Keep these separate from loans. A loan ends when the balance hits zero. A monthly deduction continues until stopped. Mixing them leads to deductions running longer than they should, or loans that don't stop when they're paid off.

How Timekeep handles loans and deductions

Timekeep tracks loans and monthly deductions separately. For loans, you enter the type (SSS salary, SSS calamity, Pag-IBIG MPL, Pag-IBIG calamity, or company), the principal, the monthly amortization, and the deduction schedule. When you run payroll, the correct amount is deducted from the right cutoff, the remaining balance decreases, and deductions stop automatically when the loan is paid off. The final deduction adjusts to match the exact remaining balance.

Back to that payroll night

The barista's SSS loan, the Pag-IBIG MPL, the cash advance. None of these are complicated on their own. The challenge is keeping all of them accurate across every cutoff, for every person, without something slipping. Set up the tracking once, and each payroll run just pulls the right numbers.

Try it free for 30 days at timekeep.ph. No credit card required.